The Capital Account (also known as financial account) is one of two primary components of the balance of payments, the other being the current account. Whereas the current account reflects a nation's net income, the capital account reflects net change in ownership of national assets.

A surplus in the capital account means money is flowing into the country. The inbound flows will effectively represent borrowings or sales of assets rather than payment for work. A deficit in the capital account means money is flowing out the country, and it suggests the nation is increasing its ownership of foreign assets.

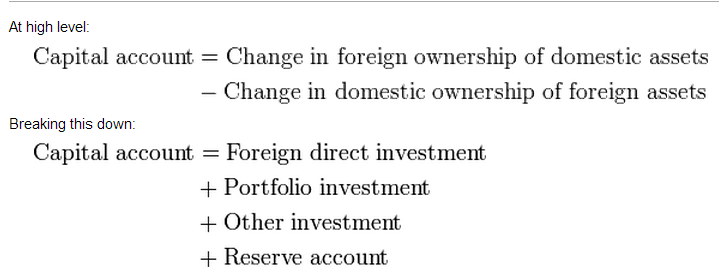

Foreign direct investment refers to long term capital investment such as the purchase or construction of machinery, buildings or even whole manufacturing plants. If foreigners are investing in a country, that is an inbound flow and counts as a surplus item on the capital account. If a nation's citizens are investing in foreign countries, that's an outbound flow that will count as a deficit. After the initial investment, any yearly profits not re-invested will flow in the opposite direction, but will be recorded in the current account rather than as capital.

Portfolio investment refers to the purchase of shares and bonds. It's sometimes grouped together with "other" as short term investment. As with FDI, the income derived from these assets is recorded in the current account(say for example, dividend); the capital account entry will just be for any buying or selling of the portfolio assets in the international capital markets.

Other investment includes capital flows into bank accounts or provided as loans. Large short term flows between accounts in different nations are commonly seen when the market is able to take advantage of fluctuations in interest rates and / or the exchange rate between currencies. Sometimes this category can include the reserve account.

The reserve account is operated by a nation's central bank to buy and sell foreign currencies; it can be a source of large capital flows to counteract those originating from the market. Inbound capital flows (from sales of the nation's foreign currency), especially when combined with a current account surplus, can cause a rise in value (appreciation) of a nation's currency, while outbound flows can cause a fall in value (depreciation). If a government (or, if authorized to operate independently in this area, the central bank itself) doesn't consider the market-driven change to its currency value to be in the nation's best interests, it can intervene.

Capital Account Convertibility

Countries without capital controls that limit the buying and selling of their currency at market rates are said to have full Capital Account Convertibility. CAC was first coined as a theory by the Reserve Bank of India in 1997 by the Tarapore Committee, in an effort to find fiscal and economic policies that would enable developing Third World countries transition to globalized market economies. In layman's terms, full capital account convertibility allows local currency to be exchanged for foreign currency without any restriction on the amount.

In a country's balance of payments, the capital account features transactions that lead to changes in the overseas financial assets and liabilities. These include investments abroad and inward capital flows. Capital account convertibility implies the freedom to convert domestic financial assets into overseas financial assets at market determined rates.

It can also imply conversion of overseas financial assets into domestic financial assets. Broadly, it would mean freedom for firms and residents to freely buy into overseas assets such as equity, bonds, property and acquire ownership of overseas firms besides, free repatriation of proceeds by foreign investors.

How far has India moved towards capital account convertibility?

Capital account convertibility is in vogue in terms of freedom to take out proceeds relating to FDI, portfolio investment for overseas investors and NRIs besides leeway for firms to invest abroad in JVs or acquisition of assets, and for residents and mutual funds to invest abroad in stocks and bonds with some restrictions. India seems to be taking the approach that easing of capital controls would be marked by removal of capital outflow restrictions on NRIs first, corporates next, followed by banks and freedom for residents in the last stage.

source: wiki, et

0 comments: